The EU’s Triangular Dilemma on Climate and Trade

Summary Points

The EU’s ambitious plans to slash greenhouse-gas emissions over the next ten years will exacerbate tensions between domestic political concerns over the economic dislocations this might cause and its international trade obligations.

The European Commission has designed a Carbon Border Adjustment Mechanism that seeks to placate domestic anxieties while being consistent with World Trade Organization law.

Simultaneously solving the EU’s climate ambitions, domestic politics, and international law, however, is an impossible task, mainly because the Paris Climate Agreement allows countries to determine their own approach to reducing carbon emissions and the World Trade Organization cannot and will not try to override this.

This triangular dilemma should not be solved through the World Trade Organization’s dispute-settlement mechanism; instead, the EU needs to do so in the context of the Paris Agreement.

The European Union has long championed global efforts to combat climate change, a campaign that has intensified dramatically since Ursula von der Leyen became president of the European Commission at the end of 2019. Yet the new proposals to achieve carbon neutrality in 30 years entail costs that will have tough political and economic consequences. To help with the politics of this, the European Commission proposed an EU “carbon border adjustment mechanism” (CBAM) that would impose costs on imports of some carbon-intensive products, although it argues this is a climate rather than trade policy measure. Whether the CBAM is used for climate, trade, or domestic political purposes, it will affect non-EU countries. They will challenge its legality under international trade law—which, even if unsuccessful, could have consequences for the EU’s climate ambitions as well as the broader international order.

This brief explores the triangular dilemma the European Commission faces in reconciling its climate ambitions, domestic political concerns about them, and international trade norms: as it solves any two sides, it will face difficulty on the third. The brief begins by describing the EU’s climate ambitions, explaining its concerns about the “carbon leakage” that the CBAM is meant to address, detailing the instrument and assessing its compatibility with international trade law, and analyzing the possible longer-term implications of the proposal.

The tragic irony is that the European Commission, in trying to mollify domestic concerns about its efforts to combat the existential threat of climate change, may undermine the climate agreement it seeks to fulfill and the international order on which the EU itself is based.

The Climate Challenge

With the world reeling from calamitous flooding, droughts, and forest fires, the European Union on June 30 adopted a Climate Law mandating that it achieve carbon neutrality by 2050. The 27 EU members must together reduce net greenhouse-gas emissions to zero in 30 years. They have empowered their citizens to take them and the policies they adopt to the European Court of Justice if they do not, as recently happened in the Netherlands.[i]

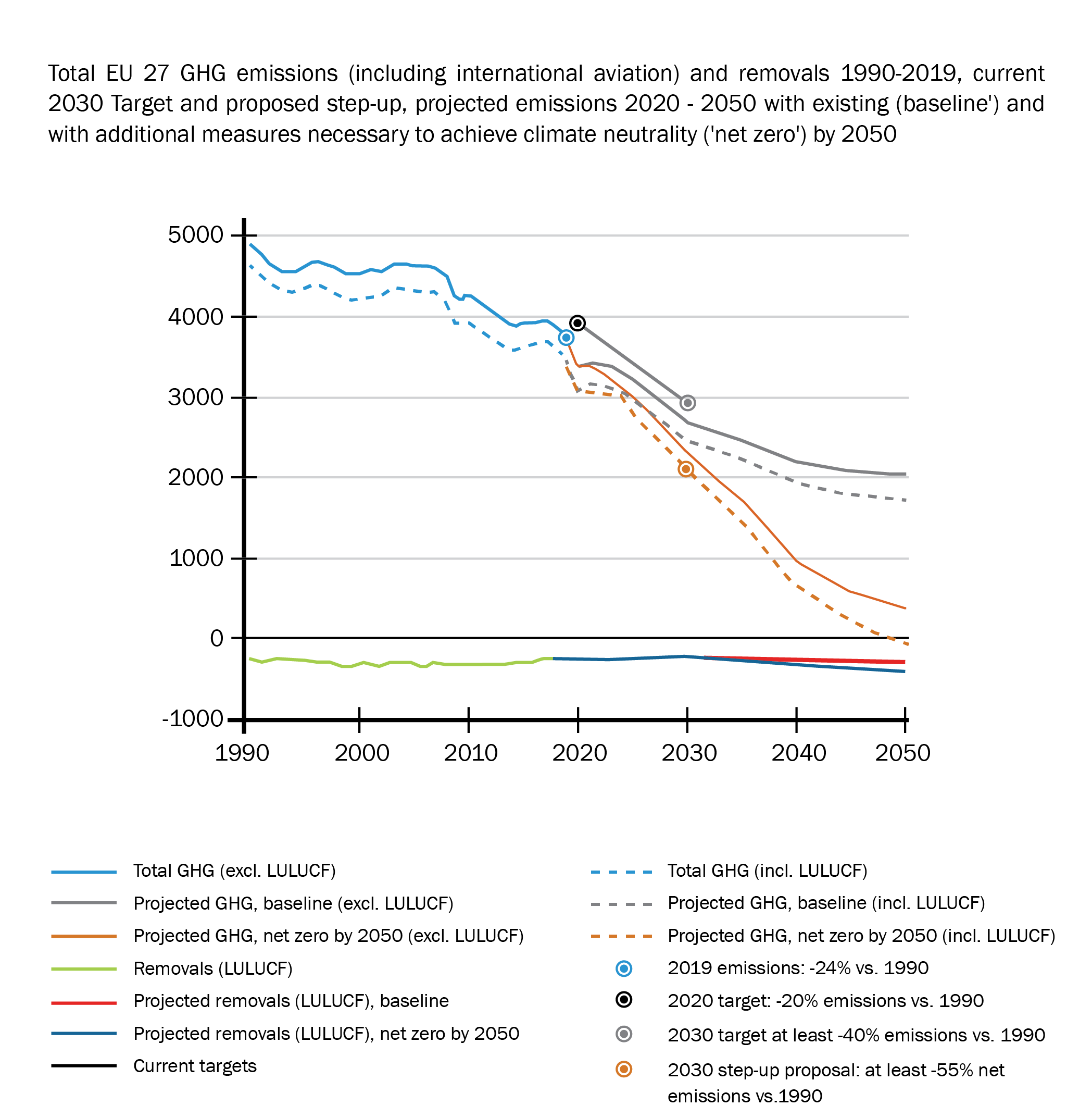

Achieving carbon neutrality will be an enormous task. It has taken the EU over two decades to reduce emissions to 24 percent below their 1990 levels,[ii] and that was relatively easy given that Europe then was powered largely by coal. As a midpoint toward the 2050 goal, the European Climate Law also includes a legally binding target of reducing emissions to 55 percent below 1990 levels by 2030—more than doubling the EU’s record of the past 30 years in only ten. Even if the member states succeed in that, as Figure 1 shows, they will still have a long way to go.

To reach the 2030 objective, the European Commission on July 14 proposed the Fit for 55[iii] package of legislative measures, which uses carbon price increases, taxes, and regulatory measures to squeeze greenhouse-gas emissions from the economy. Specifically, it proposes to:

- Slash the 2030 “cap” for CO2 emissions from the 11,000 power-generating and industrial facilities now subject to the EU’s Emissions Trading System (ETS) from about 1.2 billion tons under the current plan (43 percent less than emissions in 2005, when the ETS started) to about 820 million tons (61 percent below 2005 levels, equivalent to the amount Germany emits today).

- Phase out free allowances under these plans (now 43 percent of total allowances), while using the CBAM for the most energy-intensive and trade-exposed industries.

- Bring maritime transport into the ETS to join EU-internal aviation (which will lose its free allowances for domestic flights and be subject to a new international emissions scheme).

- Subject road transport and buildings to a new ETS for fuel suppliers, enforced by charges on fuel at the pump and for building heating (other than district heating, which is covered by the ETS).

- Increase the minimum excise tax on energy by revamping the two-decade old Energy Tax Directive so that member states tax the dirtiest fossil fuels at a minimum rate of €10.75 per gigajoule, while natural gas and first-generation biofuels are taxed at 75 percent of that, sustainable biofuels half, and electricity, advanced biofuels and clean hydrogen €0.15 per gigajoule (that is, almost nothing);

- Virtually eliminate cars and vans that run on gas or diesel from European roads by 2050 by setting fleet CO2 emission standards to zero as of 2035; and at the same time mandate that member states provide the necessary infrastructure for electric and hydrogen-powered vehicles.

- Sharply increase the targets for renewable energy (which now accounts for about 20 percent of all energy and 34 percent of electricity) from 32 percent of energy used by 2030 to 40 percent, with major inducements to the cleanest renewable fuels, including in transport.

- Create new sustainable-fuel requirements for the maritime and aviation sectors (including mandating that airlines increase their use of sustainable aviation fuels to 5 percent by 2030 and 63 percent by 2050).

- Step up member state’s greenhouse-gas emission obligations (which cover everything not under the ETS) from 30 percent below 2005 levels to 40 percent below.

- Require member states collectively to improve energy efficiency by 9 percent over 2020 levels.

The European Commission’s efforts to spell out what will be required to achieve carbon neutrality by 2050 underscore just how tough the challenge will be. European leaders know this, but argue the EU was able to reduce overall emissions by nearly 25 percent up to 2020 even as its economy grew over 62 percent.

EU leaders know that implementing these plans implies massive structural change—with all the societal and political turmoil that might entail. This is why they stress that change brings opportunity as well as challenge: the European Green Deal will also create jobs and growth in renewable energy, insulating old buildings and constructing new ones, and producing new clean cars. But, even with these opportunities, the pain of adjustment will be hard for many.[iv] So they will also fund a Just Transition Mechanism and may create the new €72 billion Social Climate Fund proposed by the European Commission using revenues generated by the ETS to support people as they adjust to this structural change away from jobs and homes associated with higher emissions to those with less.

Carbon Leakage

The tension between achieving climate goals and avoiding domestic upheaval also has an international aspect—not least as the EU is the world’s largest importer and exporter. As the price of carbon emissions increases, European governments fear industry will move factories to countries with lower carbon prices, European companies fear import competition from those countries, and European environmentalists fear global emissions increasing because of moving factories and increased imports.

Until recently, the EU has assuaged these fears about “carbon leakage” essentially by neutralizing its own restrictions—in particular, by granting free ETS allowances to protect exposed industries and aviation, which is handled separately, from the bite of an increased carbon price. This is one reason the European Commission, in its proposals, admits there is little evidence carbon leakage has taken place. But even if there is no ex post “proof” of carbon leakage, it argues that other studies show the probability of carbon leakage if carbon prices in energy-intensive trade-exposed industries rise sufficiently.[v]

The Fit for 55 proposals are explicitly designed to cause a significant increase in the price of carbon emissions in the EU, and the European Commission expects an ETS CO2 price of €60-80 by 2030 (in constant 2015 terms), up from a baseline of €26 in 2021, as a result.[vi]

This leakage effect is reflected in the modeling the European Commission conducted as it prepared its Fit for 55 package, which shows that—if the EU adopts emissions reduction measures along the lines noted above and strengthens this by eliminating all free allowances (which are provided to offset leakage)—by 2030 imports in the most energy-intensive sectors (iron and steel, cement, fertilizer, and aluminum) would be up by 10 percent over the baseline, while domestic production will have declined by 4 percent. However, the model also suggests that, while EU emissions in these sectors will be 17.1 percent below the baseline in 2030 (about 65 million tons of CO2 equivalent), those from the rest of the world would be up by 0.6 percent, or 26 million tons, suggesting a “carbon leakage rate” of 42 percent but no net increase in global emissions.

This last is true even at the sectoral level: in each of the energy-intensive trade-exposed sectors investigated by the European Commission, the increase in emissions in the rest of the world is less than the expected decline in EU emissions, although in the case of fertilizers—where EU production technology is more efficient than in most of the rest of the world—the global increase in emissions nearly offsets the EU decline.[vii] While the EU thus has a reasonable concern that other countries will produce things its factories may not be able to do as the EU price of carbon increases, its own data puts it on shakier ground in arguing that global emissions will increase.

The Carbon Border Adjustment Mechanism

Precisely because it affects the rest of the world, the European Commission has carefully designed the carbon border adjustment mechanism to offset this carbon leakage. It knows other countries will see this measure as imposing costs on their exports to the EU. If they complain that this unfairly detracts from their exports and thus their growth, this blemishes the EU’s climate leadership narrative. It could also give others an excuse to levy similar charges on imports, which the EU—as the world’s largest exporter—wants to avoid. But, more existentially, the EU is itself a creation of international law, and in a way it needs to act consistently with it. A successful challenge to its climate measures, under international trade law or any other legal regime, would weaken the EU’s legitimacy as well as its climate program.

Therefore, the CBAM:

- is tied exclusively to the ETS, rather than attempting to reflect the broader costs the Fit for 55 package as a whole will impose on the EU economy

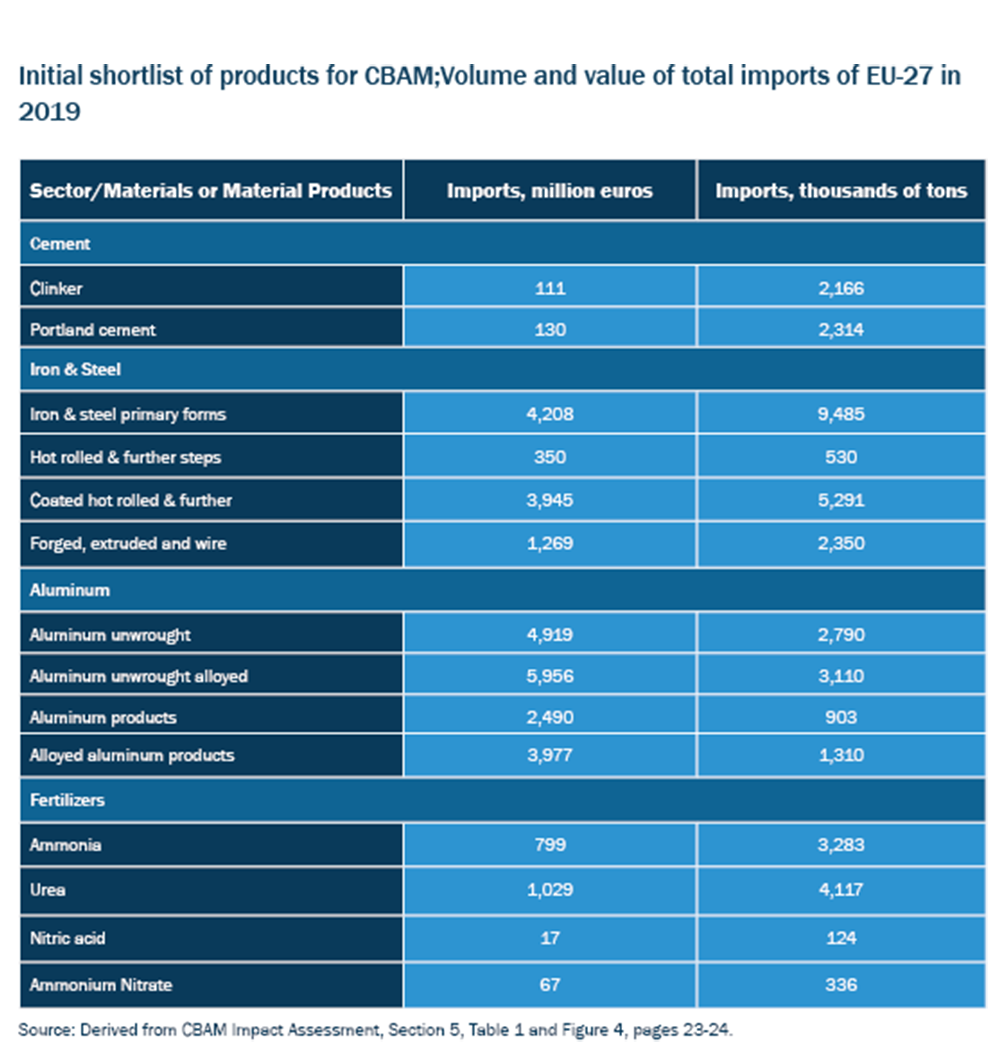

- applies initially only to four sectors (iron and steel, cement, fertilizers, and aluminum) that are covered by the ETS, account for a large proportion of emissions, face high levels of imports, and produce easily identifiable basic materials and products for which reference values of embedded carbon can be determined

- is designed to ensure only that “imported products are subject to a carbon price equivalent to the one they would have paid under the ETS, if they had been produced in Europe”

- mandates that importers pay that carbon price through the purchase of emissions certificates based on the carbon embedded in the product rather than as a duty charged at the border or an excise tax, with no limit on the number of import certificates that can be purchased

- ties the price of the import certificates to the weekly average market price of ETS carbon allowances

- allows the price to be offset by carbon prices paid in the producing country

- targets products from individual facilities rather than countries, allowing the latter to demonstrate actual embedded carbon levels, while providing an alternative “default” value based on European production site average emissions,[viii] which allows foreign suppliers with lower carbon-intensity production processes to receive credit for that and incentivizes technology upgrading while letting others use a default that provides relatively generous reference values based on European production technologies

- allows for a three-year adjustment period in which emissions certificates for imported products are provided for free as importers prepare for gathering information about actual embedded carbon levels from their foreign suppliers

- avoids “double protection” of EU industry by phasing in the CBAM in parallel with the phasing out of ETS free allowances in the covered sectors

- applies to products from all countries, regardless of level of development, on the premise that “neither the EU nor the (developing) trading partners would have an interest in fostering the growth of carbon-intensive industries in these countries.”[ix]

The CBAM’s Trade Impact

In part to minimize its trade effects, the European Commission used a very deliberative process to identify and narrow down the sectors and products covered by the CBAM.[x] Of the 50 industrial sectors and 13 sub-sectors identified under EU law as being at risk of carbon leakage in the ETS,[xi] it took only the four noted above. But these four account for 47 percent of the industrial greenhouse-gas emissions covered by the ETS: iron and steel at 22.8 percent, cement at 17 percent, fertilizers at 5 percent and aluminum at 2 percent. Among the biggest emitting sectors not included were refineries (19 percent), chemicals (13 percent over three sub-groups), pulp and paper (4 percent), glass and ceramics (4 percent).[xii]

Further, the European Commission targets only “basic materials” and “material products,” which “consist overwhelmingly of a single basic material and are usually produced in a process closely coupled and performed in the same installation as the basic material.” Materials that are highly diverse and complicated downstream products are excluded as determining carbon reference values for these is difficult and the relative price of the embedded carbon increasingly minor. The European Commission allows for expanding the scope of sectors and products covered as the process for measuring embedded carbon improves and the price of carbon increases.

As a result of this winnowing process, the CBAM would initially cover only about 2 percent of EU imports, although the absolute value is still significant, at €29.3 billion in 2019. The values are particularly large for aluminum (€17 billion) and iron and steel (€9.8 billion), while 2019 imports of fertilizers (€1.9 billion) and fertilizer (€241 million) are much smaller. This concentrated focus also helps in terms of administration as the European Commission believes these values only concern 1,000 traders and 239,000 import transactions on an annual basis from 510 production sites outside the EU.[xiii]

Nonetheless, several countries that export to the EU will be unhappy. Russia, as the largest exporter of iron and steel, aluminum, and fertilizers will be particularly hard hit—about €8 billion of its exports to the EU will be affected. Ukraine, as the second-largest exporter of iron and steel and of cement, also has grounds for concern, as does Turkey (third on iron and steel and first on cement). Other major countries affected include China (iron and steel and aluminum); the United Kingdom (iron and steel; aluminum, fertilizer); Brazil and South Korea (steel); the United Arab Emirates and Mozambique (aluminum); Egypt and Algeria (fertilizer); and Belarus, Colombia, Algeria, and Morocco (cement).[xiv] While the European Commission stresses that less developed countries only provide 0.1 percent of EU imports in iron and steel, fertilizers, and cement, it also notes that the CBAM impact will be relatively great for Senegal (cement) and Mozambique. This is particularly true for the latter: the EU takes 54 percent of Mozambique’s aluminum exports, which account for over 7 percent of the country’s GDP.

WTO Compatibility

Any of these countries could choose to challenge the CBAM under World Trade Organization (WTO) laws, as all are members and the mechanism will impose a cost on their exports to the EU. In April, Brazil, China, India, and South Africa expressed “grave concern” about possible trade barriers from a unilateral carbon border adjustment.[xv] A complaint could well be helped by the fact that the European Commission as recently as 2018 expressed doubts about the WTO-compatibility of a carbon border adjustment.[xvi]

The CBAM proposal and supporting analysis does not directly address the issue, other than by asserting that it is WTO-compatible. To do otherwise would have just given fodder to possible complainants. However, many of the CBAM features are clearly designed to ensure such compatibility. Most indicative of this is the discussion in the impact assessment on the “Options Discarded at an Early Stage”—three of the four mentioned were not considered precisely because of their incompatibility with WTO law. They are:

- imposing an additional customs duty that would exceed the EU’s schedule of commitments under Article II of the WTO’s 1995 General Agreement on Tariffs and Trade (GATT);

- applying the ETS directly to products imported into the EU, as “putting a cap on imports (as is done under the ETS) would create unacceptable restrictions on global trade” and contravene the GATT Article XI prohibition of quantitative restrictions; and

- imposing a domestic carbon tax with reimbursement of the tax on exports, as the “inclusion of refunds of a carbon price paid in the EU would undermine the global credibility of EU’s raised climate ambitions and further risk to create frictions with major trade partners due to concerns regarding compatibility with WTO obligations.”[xvii]

That said, the CBAM could easily run afoul of the WTO. International trade law, dating from the original 1948 GATT and maintained in the 1995 WTO GATT, is based on two cardinal precepts. First, a WTO member cannot discriminate among other members: the “most favored nation” principle. Enshrined in GATT Article I, it means that, while an imported product can be charged a tariff on entry, that duty should be applied equally to all supplying countries and cannot exceed the level set in the importing country’s tariff commitments under Article II. Second, once imported, a product that meets the importing country’s regulatory requirements cannot be discriminated against, as provided under the “national treatment” principle in GATT Article III.

The CBAM will clearly impose an additional cost on imported products. The European Commission estimates that the implied tariff it will levy on imported products in the four affected sectors is 3.6 percent, including 9.8 percent on cement, 7.5 percent on fertilizer and 4.2 percent on iron and steel.[xviii] As noted above, this could violate GATT Article II, including its prohibition, in paragraph 1(b), on additional “duties or charges of any kind imposed on importation” (that are not on the schedule). That article, however, in paragraph 2(a) does allow an importing country to impose additional taxes or charges on an imported product, provided those fees are also imposed on domestic products in line with the national treatment principle, as described in Article III(2), which states that imported products “shall not be subject, directly or indirectly, to internal taxes or other internal charges of any kind in excess of those applied, directly or indirectly, to like domestic products.” It goes on to say that WTO members may not impose internal taxes or other internal charges to imported products in a way that affords protection to domestic industry.

Much of the analysis about the WTO compatibility of any carbon border adjustment mechanism revolves around the jurisprudence on the GATT’s Articles II(2)(a) and III(2).[xix] One of the key issues is whether a carbon fee is a “direct” tax on companies or an “indirect” tax on products (like a value-added or excise tax). Under the WTO, only the latter can also be imposed on imports under Article II(2)(a). The WTO’s Subsidies Agreement also allows those indirect taxes to be reimbursed when a product is exported. Another key issue is whether a mechanism can distinguish between “like” products based on carbon intensity. For example, steel produced in a blast furnace competes with steel made using the electric arc process, and both face the same duty—from a trade-law perspective, justifying differential treatment based on how much carbon is emitted when the product is made is difficult. Some also question whether a mechanism can be considered a tax or a charge fixed by governments, when companies can generate income by selling emissions permits and the price of the allowances is market-determined.

In part to avoid questions like these, and because the European Court of Justice has already ruled that the ETS is not a tax precisely because it is market-based,[xx] the European Commission in its proposal appears to have taken a different route to WTO compatibility.

As noted above, one of the most fundamental precepts of international trade law is that imported products must meet domestic regulatory requirements. Article III(4) of the GATT allows for that, although it is phrased differently: imported products shall “be accorded treatment no less favorable than that accorded to like products of national origin in respect of all laws, regulations and requirements affecting their internal sale, purchase, transportation, distribution or use.” In that sense, because things made in the EU reflect the price of the cost of carbon through the ETS, imported products can as well; the CBAM in principle need not treat them less favorably.

This is one reason why the European Commission has tied the CBAM so closely to the ETS by:

- limiting the scope only to ETS-affected sectors;

- specifically identifying individual upstream products in those sectors that will be affected and avoiding more complicated downstream value chains,

- addressing only imports and not proposing to rebate ETS costs on exports, as many European industries would like;

- not limiting the quantity of emission certificates available for imports;

- requiring importers to “buy” and surrender emissions certificates on an annual basis much like the ETS;

- mirroring the ETS price;

- taking a facility-based approach that allows individual foreign installations to prove they have lower emissions than the default values;

- setting those defaults based on EU averages so that a foreign supplier cannot claim to be treated unfairly compared to a specific European producer; and

- covering all countries without exception.

The fundamental problem is that GATT law applies to products while the ETS law applies to production processes. The European Commission’s impact assessment goes to great lengths to explain how, in the four specific sectors identified for inclusion under the CBAM, one can translate emissions costs imposed within the EU on a production process to an approximation of the emissions costs associated with a product that comes out of that process. However, as it notes, “there are no rules for going into more detail (for example, splitting fallback sub-installations into more disaggregated product-specific values), and even some of the defined product benchmarks do not provide sufficient detail to assign them to the single products covered by the benchmark.”[xxi] These practical difficulties highlight the tensions in trade law between product and process issues, because in drafting the language on Article III(4), WTO members were specifically trying to avoid a situation where a country could levy additional costs on imports just because its own firms had to comply with its rules governing how things are made.[xxii] Imported products have to meet all the importing country’s regulatory and safety requirements, but the foreign firms that make those products do not have to adhere to the importing country’s labor or other general regulations. This makes the CBAM’s compatibility with the WTO questionable, despite the European Commission’s efforts.

The EU will thus need to fall back on WTO exceptions to defend its imposition of the CBAM costs on imports. GATT’s Article XX allows for such exceptions; for example, where they are necessary to protect human, animal, or plant life (paragraph 2(b)), or to protect exhaustible natural resources (paragraph 2(g)). The ETS and CBAM measures seem to be good candidates to fall within one or both of these provisions, especially as the EU has gone to great lengths to make the CBAM about the environment rather than protecting the competitive position of European industry, despite the higher ETS costs it will face. The decision not to portray the CBAM as an indirect tax that could be reimbursed on export stands out in this regard, as does the decision to reject granting special treatment to developing countries on climate grounds. (If the EU uses the revenues generated by CBAM for non-climate purposes, that would weaken its argument.)

But Article XX also requires that measures not constitute an “arbitrary or unjustifiable discrimination between countries where the same conditions prevail, or a disguised restriction on international trade.” This has been difficult to meet for countries hoping to use the exceptions clause for environmental purposes, in part as the WTO’s Appellate Body has found that countries cannot “require other Members to adopt essentially the same comprehensive regulatory program, to achieve a certain policy goal, as that in force within the Member’s territory, without taking into consideration different conditions which may occur in the territories of those Members.” A complaining country could, for instance, easily argue that using an emissions price generated by the EU market is discriminatory as it reflects very specific EU supply and demand conditions. The WTO, however, is not politically deaf, and both Panel and Appellate Body members will be conscious of the climate change challenge and the Paris climate agreement when reviewing any dispute over the CBAM.

The Paris Challenge

The Paris climate agreement could well prove a problem for the EU in the WTO. It reflects a compromise reached by 196 UN members and one of its core tenets is that, while all countries will strive to achieve the common goal of limiting the global temperature rise to 1.5-2.0 degrees Celsius, they will do so in accordance with their own nationally defined plans. Russia, China, India, Turkey, Ukraine, and other countries that will be affected by the CBAM will be able to cite the agreement in arguing that it is a disguised barrier to trade that cannot benefit from the exception under Article XX because it does not recognize their different conditions as international climate law demands.[xxiii] Even recycling some of the CBAM revenues to help these countries address their climate-change needs is unlikely to assuage them—not least as the EU has already pledged that support and providing it with funds raised on their exports is unlikely to be appreciated.

Resolving the Triangular Dilemma

The EU understands that addressing climate change requires tough measures. To its credit, the European Commission under President von der Leyen has had the courage to spell out what these measures might mean. For many, the measures may not go far enough. But many Europeans will blanch as they see the very real economic costs and social consequences. The politics of fighting climate change will not be easy.

In its Fit for 55 package, the European Commission has proposed instruments to mitigate these costs, hoping to build and retain the political support that will be needed to take these steps. The CBAM is one of these, meant to assure European firms and workers that their sacrifice will not simply be lost to imports. It has been carefully crafted, in part to ensure its legitimacy and acceptance under international trade law, even though narrowing its scope may well have weakened its impact in the domestic political debate. That it may fall on climate grounds is ironic. But it seems that no matter how one pushes and pulls at the various parts of this, there will be a triangular dilemma as domestic politics, trade law, and climate objectives will remain in tension with one another.

This dilemma cannot and should not be resolved in the WTO and under international trade law. It needs to be thrashed out in the context of the Paris climate agreement. If the parties to the Paris Agreement allow the EU, US, Canada and others to have a bit of an adjustment like CBAM to offset truly ambitious efforts to reduce greenhouse gas emissions, then the WTO would accept this. The EU needs to convince other countries that they must either undertake more serious abatement efforts in the high-emission sectors targeted (in which case, the CBAM will not be needed) or allow it (and others) to have the border buffers needed to maintain domestic political support for achieving global climate goals.

This will not be easy, and will require an intensive diplomatic effort, something the European Commission pledges to do in its CBAM proposal. If the proposal provides some of the leverage it will need for its effort, then maybe that will prove its main contribution.

[i] Supreme Court of the Netherlands, Judgement 19/00135 in the matter between the State of the Netherlands and Stichting Urgenda, December 20, 2019.

[ii] European Commission, EU Climate Action Progress Report, November 2020, p. 1.

[iii] European Commission, ‘Fit for 55’: delivering the EU's 2030 Climate Target on the way to climate neutrality, July 14, 2021.

[iv] See the Impact Assessment accompanying the European Commission Staff Working Document, Climate Target Plan 2030, September 17, 2020, especially Sections 6.4 and 6.5 on the economic and social impacts of various policy options, pp. 65-92.

[v] European Commission Staff Working Document, Impact Assessment Report accompanying the Proposal for a Regulation Establishing a Carbon Border Adjustment Mechanism (CBAM Impact Assessment), July 14, 2021, Annex 11, p. 115. The European Commission also cites Andrew Prag, Climate Policy Leadership in an Interconnected world: What Role of Border Carbon Adjustments? Organization for Economic Co-operation and Development, February 25, 2020, paragraph 30.

[vi] European Commission Staff Working Document, Impact Assessment Accompanying the Proposal for a Directive Amending the EU Emissions Trading System, July 14, 2021, Volume 2, Annex 4, Table 36, p. 64 and Table 45, p. 91. In reality (as opposed to the models), the July 2021 price is above €50, so the model projected price for 2030 should be much higher.

[vii] Impact Assessment accompanying the European Commission Staff Working Document, Climate Target Plan 2030, September 17, 2020, pp. 46-47. The “carbon leakage rate” is the ratio between the change in emissions in the rest of the world (ROW) divided by the change in EU emissions as a result of the EU implementing its Fit for 55 package and ending free allowances. Positive values greater than 100 percent would be “true” carbon leakage, as they imply a net increase in global emissions as ROW emissions increases exceed the decline in EU emissions. Positive values less than 100 percent indicate that ROW emissions increase, but less than the EU decline. Negative values imply a global reduction in CO2 levels as emissions from the ROW also decline because they are not filling EU demand or improving technology.

[viii] The default is initially at the median level and then, after a transition, at the average of most carbon intensive European producers.

[ix] Many of these design features are discussed in Aaron Cosbey et al, Developing Guidance for Implementing Border Carbon Adjustments: Lessons, Cautions, and Research Needs from the Literature, Review of Environmental Economics and Policy, Vol. 13(1), 2019. Impact Assessment accompanying the European Commission Staff Working Document, Climate Target Plan 2030, September 17, 2020, p. 30.

[x] Ibid, Annex 7, pages 231-264 of the pdf file. The numbering of the pages in the Annex is severely corrupted.

[xi] Commission Delegated Act 2019/708, February 15, 2019.

[xii] Sectors not included may clamor for some form of protection from imports; for a detailed discussion of the largest emitting sectors and a border adjustment, see Andre Marcu, Michael Mehling and Aaron Cosbey, Border Carbon Adjustments in the EU: A Sectoral Deep Dive, European Roundtable on Climate Change and Sustainable Transition (ERCST), March 18, 2021.

[xiii] Ibid, page 28, pdf pages 108-109.

[xiv] Ibid, Annex 10, pdf pages 275-276.

[xv] Joint Statement Issued at the Conclusion of the 30th BASIC Ministerial Meeting on Climate Change Hosted by India on April 8, 2021, Government of South Africa.

[xvi] Staff Working Document, In-Depth Analysis in Support of A Clean Planet for All: A European Long-Term Strategic Vision for a Prosperous, Modern, Competitive and Climate-Neutral Economy, European Commission, November 28, 2018, page 263.

[xvii] Impact Assessment accompanying the European Commission Staff Working Document, Climate Target Plan 2030, September 17, 2020, p. 42.

[xviii] Ibid. Annex 10, p. 114.

[xix] See the bibliography for some of the studies consulted on the WTO compatibility issue.

[xx] Court of Justice of the European Union, Case C-366/10, Air Transport Association of America, American Airlines, Inc, Continental Airlines, Inc, United Airlines, Inc v The Secretary of State for Energy and Climate Change, 21 December 2011, ECLI:EU:C:2011:864, para 143.

[xxi] See Impact Assessment accompanying the European Commission Staff Working Document, Climate Target Plan 2030, September 17, 2020, Annex 7, Sections 3(b) and (c) and Section 4. Quote at p. 248.

[xxii] For a review of this issue and relevant WTO jurisprudence, see Reinhard Quick, Carbon Border Adjustment: A Dissenting View on its Alleged WTO-Compatibility, Nomos E-library, April 2020.

[xxiii] Uri Dadush, The EU’s Carbon Border Tax is Likely to Do More Harm Than Good, Policy Center for the New South, June 2021.

Bibliography

James Bacchus, When Two Global Agendas Collide: How the EU’s Climate Change Mechanism Could Fall Afoul of International Trade Rules, World Economic Forum, July 7, 2021.

Camilla Bausch, Bridging Divides Over the Carbon Border Adjustment Mechanism, Ecologic, April 14, 2021.

Julien Bueb et al, Border Adjustment Mechanisms: Elements for Economic, Legal and Political Analysis, World Institute for Development Economics Research, April 2016.

Aaron Cosbey et al, A Guide for the Concerned: Guidance on the Elaboration and Implementation of Border Carbon Adjustment, Entwined Policy Report, November 21, 2012.

Uri Dadush, The EU’s Carbon Border Tax is Likely to do More Harm than Good, Policy Center for the New South, June 2021.

European Parliament, European Parliament Resolution toward a WTO-Compatible EU Carbon Border Adjustment Mechanism, March 10, 2021.

Brian Flannery et al, Policy Guidance for US GHG Tax Legislation and Regulation: Border Tax Adjustments for Products of Energy-Intensive, Trade-Exposed and Other Industries, Resources for the Future, October 23, 2020.

Jennifer Hillman, To Address Climate Change while Protecting Workers, the United States Needs a Border-Adjusted Carbon Tax, Council on Foreign Relations, November 13, 2020.

Jennifer Hillman, Changing Climate for Carbon Taxes: Who’s Afraid of the WTO, German Marshall Fund of the United States, July 25, 2013.

Kateryna Holzer, WTO Law Issues of Emissions Trading, World Trade Institute, April 2016.

Henrik Horn and Petros C. Mavroidis, To B(TA) or Not to B(TA)? On the Legality and Desirability of Border Tax Adjustments from a Trade Perspective, SSRN, December 20, 2011.

Alexxander Krenek, How to Implement a WTO-Compatibvle Full Border Carbon Adjustment as an Important Part of the European Green Deal, Österreichische Gesellschaft für Europeapolitik, January 20, 2020.

Johanna Lehne, The EU Can’t ‘Go it Alone’ on Border Carbon Adjustments, E3G, October 8, 2020.

Sam Lowe, The EU’s Carbon Border Adjustment Mechanism: How to Make it Work for Developing Countries, Centre for European Reform, April 22, 2021.

Ben McWilliams and Simone Tagliapietra, Carbon Border Adjustment in the United States: Not Easy, but Not Impossible Either, Bruegel, February 11, 2021.

Michael Mehling et al, Designing Border Carbon Adjustments for Enhanced Climate Action, Climate Strategies, December 2017.

Joost Pauwelyn and David Kleimann, Trade-Related Aspects of a Carbon Border Adjustment Mechanism, European Parliament, April 2020.

Reinhard Quick, A Carbon Border Tax or a Climate Tariff, International Law and Policy Blog, October 2019.

Reinhard Quick, Carbon Border Adjustment: A Dissenting View on its Alleged GATT-Compatibility, Nomos eLibrary, June 2020.

André Sapir, The European Union’s Carbon Border Mechanism and the WTO, Bruegel, July 19, 2021.

Harro van Asselt and Michael A. Mehling, Border Carbon Adjustments in a Post-Paris World, Same Old, Same Old, but Different?, SSRN, June 5, 2020.

George Zachmann and Ben McWilliams, A European Carbon Border Tax: Much Pain, Little Gain, Bruegel, March 2020.