Transatlantic Cooperation on Semiconductors

The strength of Western and Western-allied companies in critical areas of the semiconductor value chain means that Western sanctions can be wielded to devastating effect and with far-reaching implications. For example, past sanctions and political pressure applied to Huawei and Semiconductor Manufacturing International Corporation (SMIC), China’s top chipmaker, reduced the revenue of the former by 29 percent and prevented the latter from acquiring the extreme ultraviolet lithography machine of Dutch company Advanced Semiconductor Materials Lithography (ASML), inhibiting SMIC’s ability to manufacture advanced chips.1 New export controls rolled out in response to Russia’s invasion of Ukraine, which target Russian access to semiconductors, related equipment, and other cutting-edge technology, similarly demonstrate the reach of the United States and the European Union when it comes to the pursuit of advanced chip capacity. While directly attacking the Russian industrial base, the controls also serve to dissuade China from filling in the gap. But while existing dominance in key areas of the semiconductor supply chain currently allows the United States and the EU to dictate terms, they risk seeing their preeminence erode as strategic rivals advance efforts to develop their own domestic industry.

To shore up their positions, the United States and Europe are each committing billions of dollars to boost domestic manufacturing, provoked by semiconductor supply shortages—stemming from a reliance on just-in-time supply chains and a decades-long practice of offshoring manufacturing—evident in the past two years, which threaten the availability of a sweeping number of consumer products, industrial equipment, and critical national security items. Although the United States and Europe have similar vulnerabilities and have publicly committed to cooperate on this effort to avoid duplicating investments, no plan yet exists to combine forces.

The United States and the EU are leaders in the most intensive R&D activities, like chip design and the underlying software and intellectual property that enable it, such as electronic design automation software and reusable architectural building blocks. In addition, the United States produces key machinery used in the production of semiconductors, like Lam Research’s plasma etching machines or Applied Materials’ eBeam metrology system for semiconductor patterning control. The EU is particularly strong in the design of components that power electronics, radio frequency, and analogue devices, and is home to world-leading suppliers of equipment, like ASML, Zeiss, and Atlas Copco. In some cases, Europe is the sole producer of equipment required to manufacture leading-edge chips, such as ASML’s extreme ultraviolet lithography technology. The EU also has dominant companies that specialize in the design of semiconductors for automotive and industrial equipment and maintains domestic access to critical raw materials such as substrates and gases

- 1The United States’ role in blocking the sale of ASML equipment was more a function of its diplomatic power than the application of a foreign direct product rule, but nonetheless demonstrates the influence and reach of US national interests across the semiconductor industry.

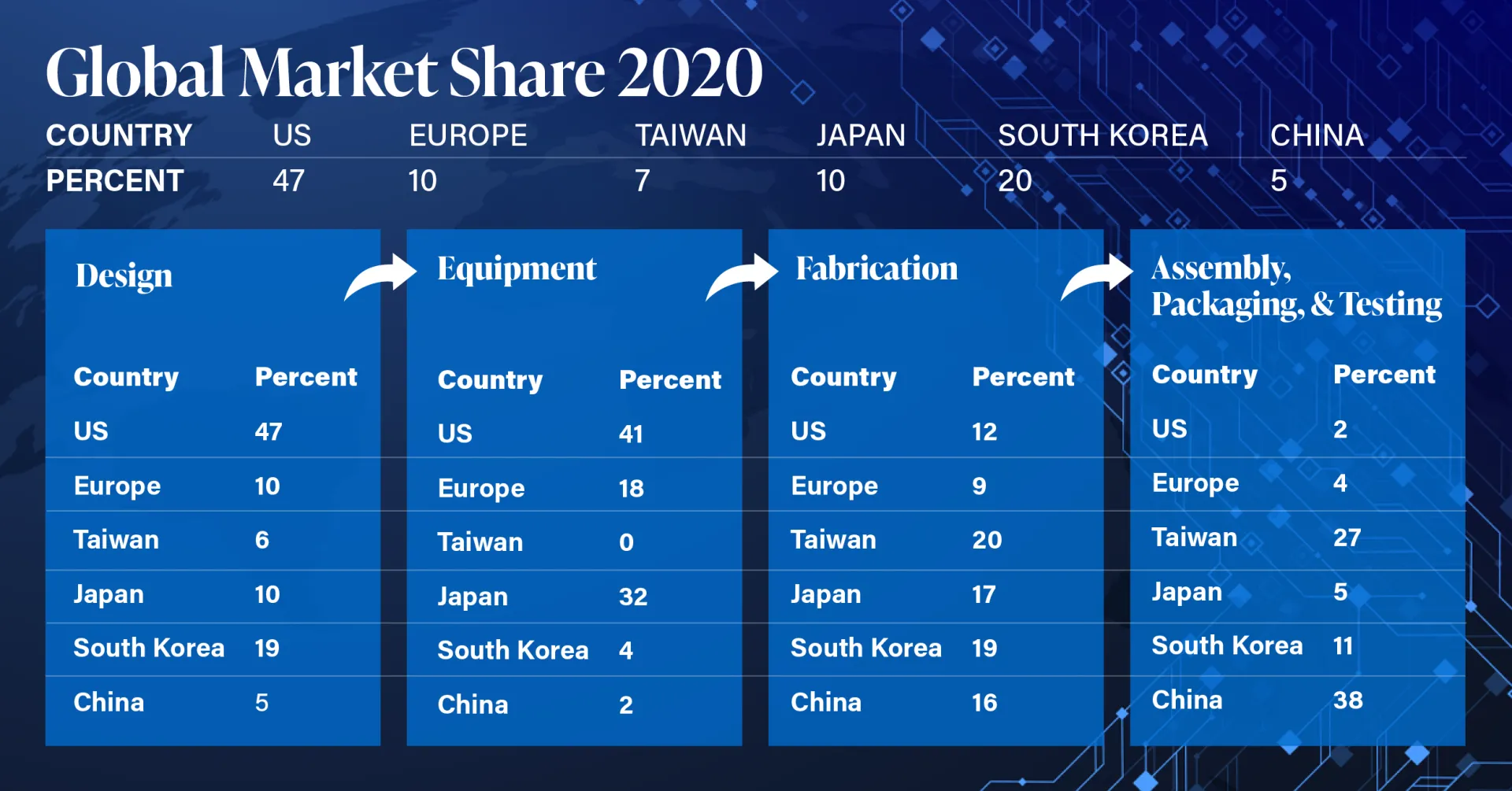

Figure 1: Statistics from the Semiconductor Industry Association’s 2021 State of the US Semiconductor Industry report and the Center for Security and Emerging Technology’s issue brief on The Semiconductor Supply Chain: Assessing National Competitiveness. N.B.: figures may not add up to 100 percent.

But while the United States and Europe combined account for over half of the manufacturing equipment value chain and more than half of the global semiconductor market share—with US and EU semiconductor companies comprising 10 of the 15 largest firms worldwide by sales in 2021—these strengths elide key deficiencies and strategic blind spots. The actual manufacturing of the chips these firms sell often occurs at foreign foundries.

The US share of modern semiconductor fabrication capacity was 12 percent in 2020, down from 13.8 percent in 2015 and continuing a long-term decline from around 40 percent in 1990. This decline is in part due to the growth of “fabless” firms, which design chips but outsource the actual manufacturing to third-party foundries. For example, out of the 10 US and European firms that are largest in terms of worldwide sales, five are fabless, relying on other companies to manufacture the chips they sell.

The US share of modern semiconductor fabrication capacity was 12 percent in 2020, down from 13.8 percent in 2015 and continuing a long-term decline from around 40 percent in 1990.

Meanwhile, Europe’s share of fabrication capacity is only 9 percent. The bloc lacks cutting-edge as well as trailing-edge (a few generations behind cutting-edge) logic fabs, and there are no foundries in Europe producing process nodes under 22 nanometers.

In fact, almost all chips under 10 nanometers are produced in Taiwan and South Korea by Taiwan Semiconductor Manufacturing Company and Samsung, and the United States is behind when it comes to logic chips that are 28 nanometers and above. Taiwan, South Korea, and Japan account for 56 percent of global manufacturing capacity, 57 percent of materials, and 43 percent of global assembly, packaging, and testing.

Taiwan, South Korea, and Japan account for 56 percent of global manufacturing capacity, 57 percent of materials, and 43 percent of global assembly, packaging, and testing.

The US and European semiconductor supply chains are brittle. Natural disasters and industrial accidents have had significant effects on supply. When deadly snowstorms hit Texas in February 2021, a number of chip firms were forced to shut down production, and a factory fire at a major Japanese supplier caused similar disruption. The Semiconductor Industry Association estimates that if Taiwan were forced to cease production for one year, the global electronics supply chain could come to a halt. If the interruption became permanent, it could take a minimum of three years and a $350 billion investment to build enough capacity in the rest of the world to replace the Taiwanese foundries. The critical materials required for the production of semiconductors, like neon and palladium, are another point of exposure—for example, Russia controls approximately 37 percent of global palladium production, and Russia and Ukraine supply 40 to 50 percent of the world’s neon gas. Overall, 73 percent of materials needed throughout the semiconductor supply chain are located in China, Taiwan, South Korea, and Japan.

In addition, although China remains behind when it comes to semiconductor manufacturing—deficient in advanced logic foundry production, electronic design automation (EDA) tools, chip design intellectual property (IP), manufacturing equipment, and materials—it is a leader in outsourced assembly, packaging, and testing (with 38 percent of world market share), and accounts for 16 percent of the global fabless semiconductor market. As part of its “Made in China 2025” industrial plan—introduced in 2015 and designed to reduce dependency on foreign technology—the government has committed enormous sums to subsidize the construction of fabrication facilities and advanced manufacturing capacity, setting a revised objective of expanding semiconductor production to meet 80 percent of domestic demand by 2030.

To achieve this goal, it has deployed a range of state support, including production targets, subsidies, reduced utility rates, tax preferences, and trade and investment barriers.2 The China Integrated Circuit Investment Fund, the vehicle for state-led investment in the semiconductor industry that was launched in 2014, has invested $39 billion, almost 70 percent of which has been for front-end manufacturing. Across the domestic semiconductor industry, 43 percent of registered capital—the maximum amount of money a company is authorized to issue to shareholders—is directly or indirectly owned or controlled by the Chinese government, illustrating the state’s influence in steering the domestic sector.

- 2For example, in August 2020, China further increased preferential tax policies for semiconductor manufacturers, including up to a 10-year corporate tax exemption.

Overall, 73 percent of materials needed throughout the semiconductor supply chain are located in China, Taiwan, South Korea, and Japan.

The United States and Europe are seeking more domestic manufacturing capacity, but it takes billions of dollars and an average of three to five years to build one manufacturing facility. Appropriations for the US CHIPS Act (which has been passed by both the Senate and House of Representatives but has not yet been enacted) allocate $39 billion to building or upgrading manufacturing facilities or equipment, both for mature and leading-edge chips. While recognizing the importance of capacity for both types of chip, the European Chips Act (which has been referred to the relevant committee in the European Parliament and would provide at least €43 billion in public and private investments) differs somewhat by prioritizing the development of manufacturing facilities which commit to investing in the next generation of chips. The US FABS Act would provide a 25 percent tax credit for investment in semiconductor manufacturing facilities or equipment.

Intel emphasized the need for legislation in announcing new investments for Ohio—a $20 billion investment in a chip factory which could increase to $100 billion over ten years—and numerous sites in Europe, including €17 billion for a fab mega-site in Germany that will produce both leading-edge chips and angstrom-class transistors, a size below nanometer. And the competitive boost provided by such investments and tax credits was championed by US semiconductor firms Micron and Intel at a recent hearing, arguing that their Asian competitors benefit from lower operating costs due in part to government investments.

By implementing the semiconductor initiatives currently pending on both sides of the Atlantic, they can ensure that such strategic power remains in their hands.

Today, when export controls are applied, the dominant market share in EDA, IP, and equipment held by the United States and the EU—and the reliance by foundries and firms in third countries on these tools—functionally serves to sever targeted states from advanced semiconductor manufacturing. By implementing the semiconductor initiatives currently pending on both sides of the Atlantic, they can ensure that such strategic power remains in their hands.

The United States and the EU will strive to work together, including through the Trade and Technology Council, to leverage their dominant position in R&D-intensive areas of the semiconductor ecosystem and shore up their strengths without entering a zero-sum subsidy contest. As the European Commission has recognized, guaranteeing a reliable global market for European products and ensuring security of supply “will require building balanced semiconductor partnerships with like-minded countries…[with the aim of setting] out cooperative frameworks on initiatives of mutual interest and seek[ing] a commitment to ensure continuity of supply in times of crisis.” The United States has similarly acknowledged the importance of formalizing cooperation with allies in the context of fostering secure supply chains, allocating $500 million over five years for the establishment of a Multilateral Semiconductors Security Fund, which includes provisions for developing harmonized export controls, intellectual property rights, and foreign direct investment screening. But more work will be needed to develop formal frameworks of collaboration that facilitate the regular sharing of supply-chain data, establish protocols and practices to detect and prepare for supply crises, create long-term investment strategies that cohere rather than conflict, and support joint international standardization efforts.